The Healthcare Breakdown No. 025 - Breaking down how insurance companies make more money than you

Brought to you by Log; it’s better than bad, it’s good

What we’re breaking down: Intercompany eliminations and the vertical integrations that make yachts possible

Why it matters: These strategies exist to maximize profit. They impact access and cost. And not in a good way.

Read time: The best scene from Cliffhanger (5 minutes for real though)

All right you beautiful souls, let’s charge straight into this one. Back on my numbers bull-hooey, so buckle up! Put on your reading glasses for the tiny 10K print and wait to go to Target for a pumpkin spice latte while you shop for one thing and end up buying 24.

I am going to start with a story to help elucidate the point before we get to our lovely insurance processors and how they use this strategy to make all the money.

When I started a medical device company, I partnered with a contract manufacturer. In fact, the contract manufacturer became the parent company of my little startup, pretty much from the jump.

One thing that made this super awesome sauce, other than claiming I was cooler than I actually was and having a bowl of little candies in the middle of a conference table, I also got first hand experience with intercompany eliminations.

Here’s how it worked:

I ordered my product from my contract manufacturer (parent company). They charged me $500 (made up number) and I sold things for $1,000 (still made up numbers). The manufacturer’s cost was $200 (guess what? I made this number up too).

Cool. I made five hundo, they cleared three.

Here’s the magic trick though. The parent company would record a $500 sale and I would record a $500 purchase.

But since we are really one company, we need to eliminate the intercompany transaction. Otherwise we would be double counting stuff. And you can’t double count stuff. It’s like saying you sold yourself a popsicle and made money selling yourself a popsicle.

See, it makes no sense. Not the popsicle. The selling things to yourself part. Popsicles always make sense.

Because you can’t sell things to yourself, we eliminate the intercompany transaction. Just cancel that sucker out.

When the rolled up P&L is reported you in essence see this: $1,000 sales, $200 cost.

My margin was $500.

Their margin was $300.

Our soup-to-nuts margin was $800.

You can also call it cradle-to-grave. Depending on whether you’re feeling hungry or macabre.

I made a picture:

Pssst… Healthcare needs you! Don’t let finance be the thing that holds you back from changing healthcare. Learn finance this afternoon for 1/535th the price from a much funnier guy than your average finance professor.

It’s Healthcare Breakdown - The Finance Course! The kids are gonna love it.

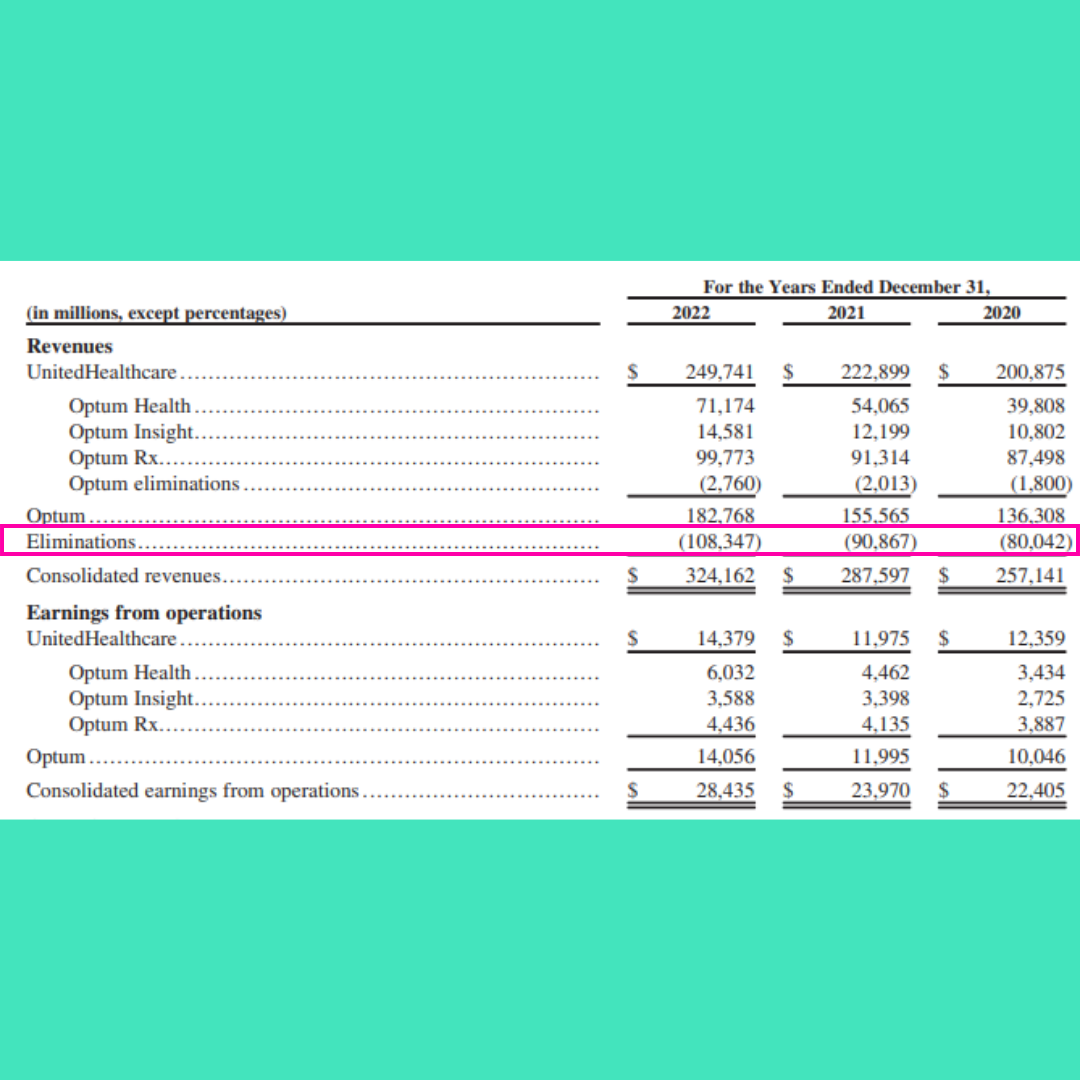

Here is how your favorite healthcare company uses this. It’s UnitedHealthcare. They’re your favorite.

But first!

Side bar.

Remember the ACA? Still a thing. One of its provisions was the Medical Loss Ratio (MLR). What that does is limits an insurance company’s ability to make profits… by percentage alone.

It requires an insurer to spend 80-85% of its premium revenue on medical claims. Obviously unintended consequences abound. One of which is the incentive for insurers to raise premiums and relish in ever increases costs of care as it is the only way to maximize profit dollars.

Well, not the only way. You’ll see.

Quick picture of the MLR:

Remember, insurers are publicly traded (mostly). They exist to maximize profit and shareholder value. They can literally be sued by shareholders if not working to maximize their value.

Yay America.

Funny story, insurers brag on earnings calls when their MLR is low.

Brag. About not providing care… that you pay for.

Anyways… I’m almost off track, but not quite. Aside from the unintended consequences, insurers need to find a way to make more money dang it!

They have this pesky MLR to contend with and lots of bonuses to pay out and stocks to buy back. There must be a way to generate more margin on operations!

Ooooh, I know, I know! Pick me! Ahem….

Vertical integration.

Why do you think UnitedHealthcare paid all the money for Optum?

Why is Optum such a huge part of the business now?

Why does every insurer have a major PBM, services organization, and clinical practice?

P to the R to the O to the F to the I to the T.

I’m practicing being a rapper for after my news-letty takes off and I can retire.

None of those other entities are bound by MLR and are free to make as much profit as they possibly can.

And if you go back to my real life with made up numbers example, you can see how it’s done.

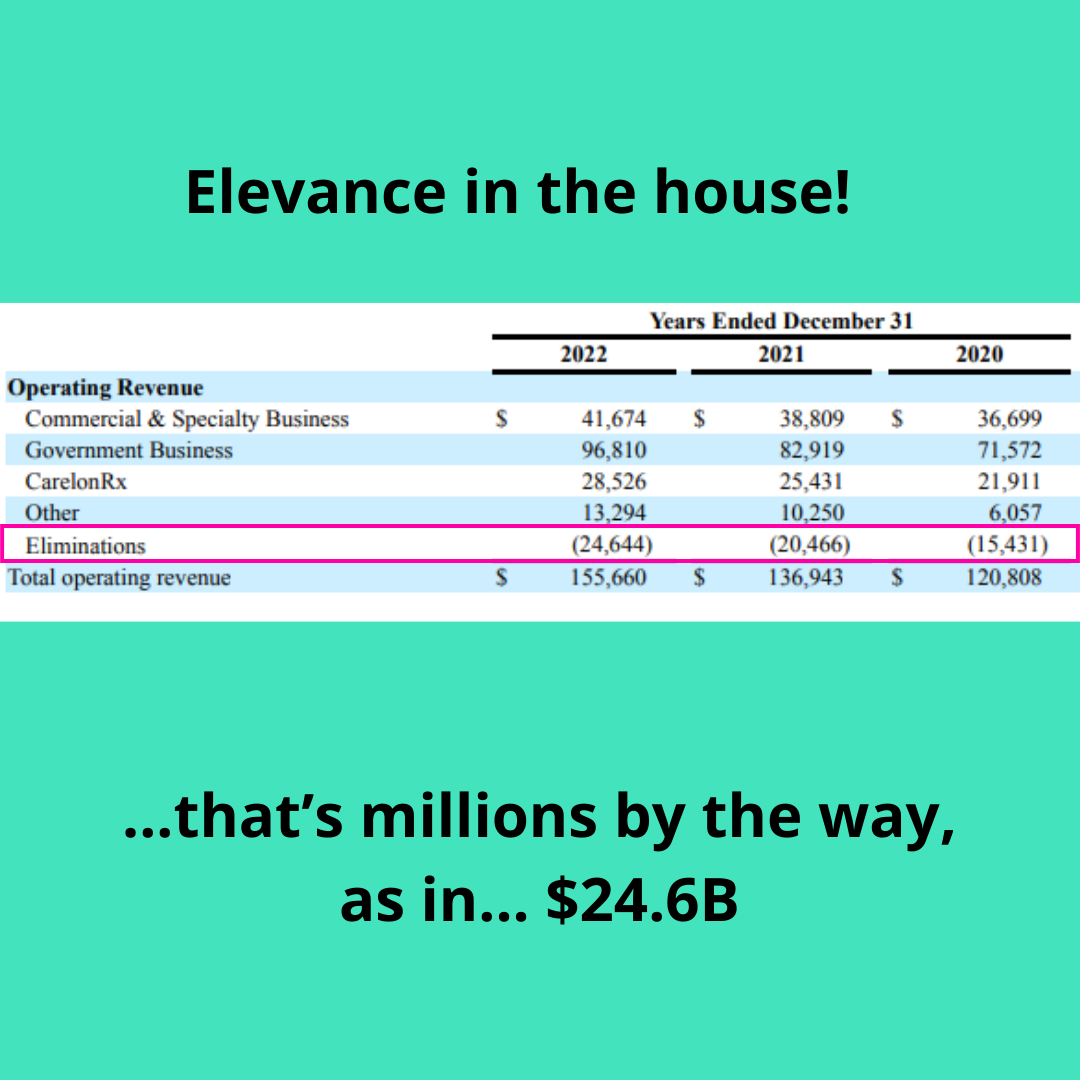

Here is the magnitude of the eliminations amongst your favorite insurers:

So like, billions of dollars. Naturally.

Here is a simplified version of how this allows the big dawgs to eat more pimento cheese sandwiches than they should be.

That was a weird metaphor….

That’s the way the cookie crumbles. To put it in words, big bad BUCAH gets $100B in premiums and spends $85B on claims.

They pay that $85B to their subsidiaries for services. It only costs the subsidiaries $60B to deliver the care.

Get out your big pink eraser and all we are left with is….

That’s it. That’s the game.

Totally legal. Totally on the “up and up.” I mean dirty for sure. Unethical perhaps. Smarmy. Gross. Lame. Total herb-tastic move (for my homies from the northeast).

But, until the FTC steps in to stop the vertical integration bonanza, this is how it’s done.

Who’s next on the vertical acquisition list?

(Please say me, please say me, please say me….)

Just kidding, I’m def not smart enough to get bought by a Fortune 5 company.

Plus, I run my mouth too much.

Adios.

P.S. If you don’t know what Log is, you weren’t a 90’s kid. But it’s cool. I totally still love you.

K, Bye.

This is one of the clearest (and funniest except for the numbers and United, etc.) explanations of these economics that I have seen. My son gets his insurance (top policy) through MD Exchange (ACA). I was in shock when I got the rebate check for MRR. But, it was not from United, Aetna, etc. if more people (and legislators understood these numbers and what are effectively vertical oligarchies), there might be hope for change...Love your newsletter!