The Healthcare Breakdown No. 067 - Breaking down where in the heck sauce is all the money in healthcare?

Brought to you by everyone loving a good comeback story

What we’re breaking down: The current landscape in healthcare funding

Why it matters: Life comes at you pretty fast and if you’re not careful, you might not be able to raise a seed round or sell your practice

Read time: The time it takes for your sourdough to rise (9 minutes for real though)

Oh Hi.

I hope that since December 18th you have missed me desperately and pined for the return of this publication. Well, here it is!

The Healthcare Breakdown is back!

Better than ever? Time will tell. But definitely back. And before we get all up in it, I’d like to take a minute, just sit right there, and I’ll tell you what’s been going on the last few months and what’s on the horizon for this periodical.

Where I’ve been

First, what I’ve been up to, since I know half the reason you read this is for my stunning personality and you are completely enthralled with my life outside this journal.

I put down the newsletter in December, because my company, Forward Slash / Health was working on launching a new SaaS platform and I was pouring a ton of energy into the launch. At the same time, my business partner, you know her – it’s Sarah Covington – had been taking on clients as one does when bootstrapping. Well, things got a little out of hand in all the best ways, she had a bevy of clients and we decided, hey, why not just make this law firm thing the real deal too. So, I also started helping run the law firm.

Strictly as a non-attorney of course. I am far too informal for that life.

The firm is Underscore _Law, it’s awesome and we do business and transaction law for healthcare startups and clinical practices. I never thought I would be in this space, but it’s fantastic to be on this side of helping startups form, launch, and continue to grow.

And a few weeks ago I was in New York for Tech Week, hanging out with some very wonderful folks, who all had very nice things to say about The Healthcare Breakdown, and I thought you know what, I am bringing it back!

It could have also been the mimosas who said that, but nonetheless it was said. And here I am.

I figure between the legal work, the finance work, the operations work in healthcare, and my uncanny ability to weave 90s references into a newsletter about healthcare, that this was the perfect time to bring back the breakdown.

So, that’s where I have been and that’s why we’re back.

Now, what’s different.

Not all that much. We’re still talking healthcare, healthcare finance, the business of healthcare, and will certainly be pulling back the curtain as to what’s really going on. But I want to take a step further to break down more mechanics that impact founders, clinicians, and investors.

Yes, knowing that United Healthcare pays itself $168B a year via intercompany eliminations so it can make the medical loss ratio a figment of its imagination, but the question was always, ok… and?

Well, here is the and. Because there is more going on in the trenches than just BUCAH shenanigans and big health systems bupkis.

And as I have stepped back into the world of startups, capital raising, M&A, and some other acronyms, I want to write more about it. The real operational and financial mechanics of healthcare that so many of us work in and are working towards.

To that end, I will be writing more about funding, fundraising, the startup ecosystem, deal mechanics, fund mechanics, and how the money continues to move in healthcare.

Yes, there will still be fist wagging. Don’t worry. But buckle up because we are still going to make all the jargon simple and breakdown healthcare so you can see what’s really going on.

Even better, so you can do something about it.

OK, if all that wasn’t enough, here’s what we’re diving into today.

It’s really a tee up to give you a flavor of the future and the next spate of issues.

We’re talking about where in the world has the money gone in healthcare daggumit! (Is that how you spell that…?)

The main part

Just to indulge myself, here’s the story that inspired this episode.

I was talking a couple weeks ago with an investor who runs a decent size VC in Nashville. Yes, that Nashville, best known as the adopted home of Queen T. He was sharing that money is tight right now for startups. The raising environment is hard for both funds and especially for startups.

And just last week I was talking with an investment banker, ya I know cool people, who was talking about raising tranches, active LPs, and deploying a ton of capital. Crushing it. I mean, the VC was too, but the tenor was different as he spoke about the environment.

Both in the flow, both with funds, but two very different perspectives and experiences.

So, what is going on? Well, both things can be true at once.

If you are a startup with anything that isn’t native “AI something something” with billing services at the core of the product after stripping back the AI candy wrapper built on someone else’s LLM, then it’s hard to raise money right now.

And if you are a physician practice out there looking for a buyer who is going to pay you 18x EBITDA, for some reason you can’t find them.

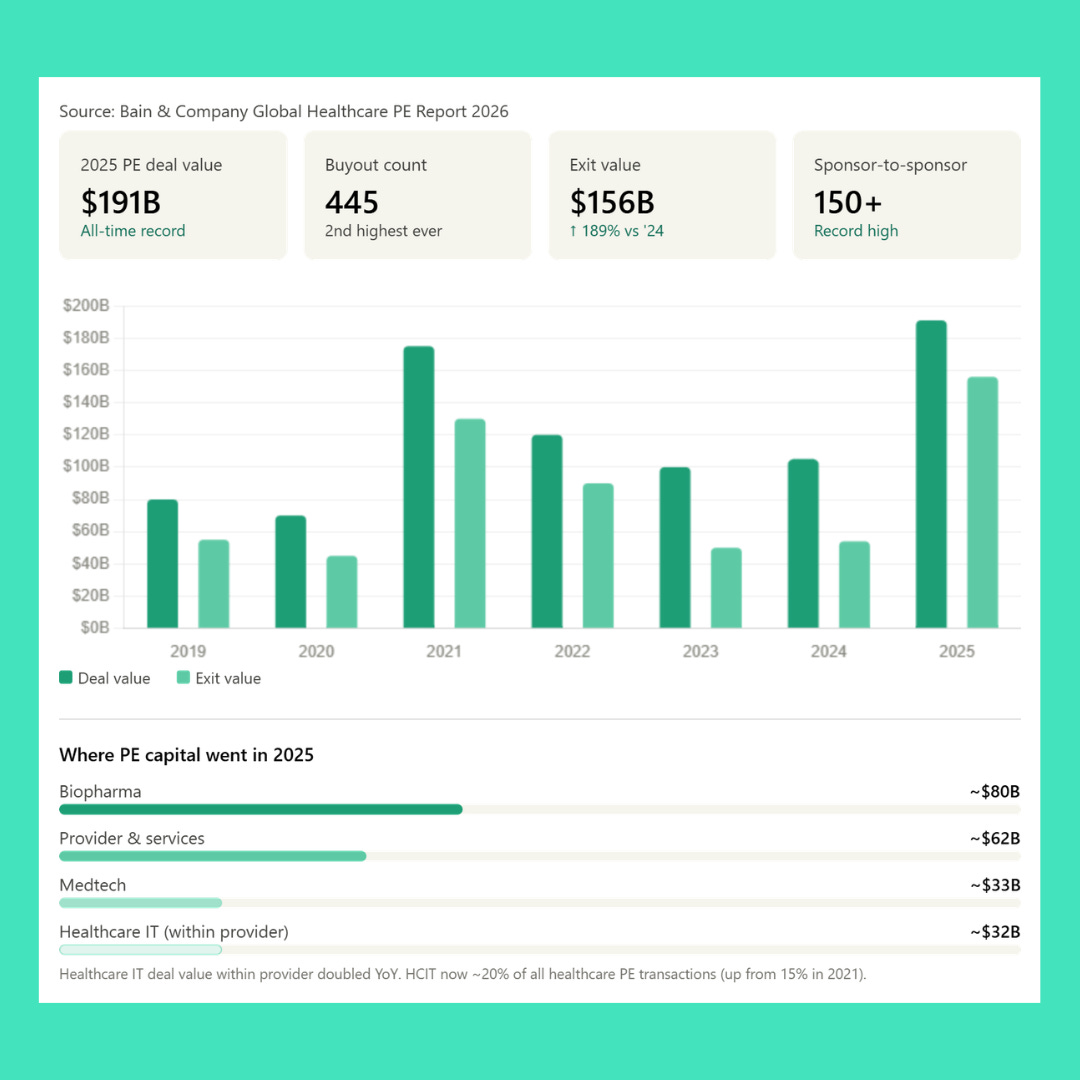

Meanwhile, we have seen a record year for Private Equity investment with over $191B in healthcare deal value in 2025, and a similarly large year for Venture Capital investments into healthcare. But of course, with everything, the devil is in the details.

Let’s check out what’s happening with Venture Capital right now.

Oh, by the way, there’s this thing these days, you may not have heard of it, it’s called Claude. I think he’s French. I have started using him to make some financial charts and graphics. Just trying to up my game on the comeback. The weird green, teal, turquoise, aqua stays though. Obvs.

Just wanted to give you a heads up based on how swanky some of these charts are going to look.

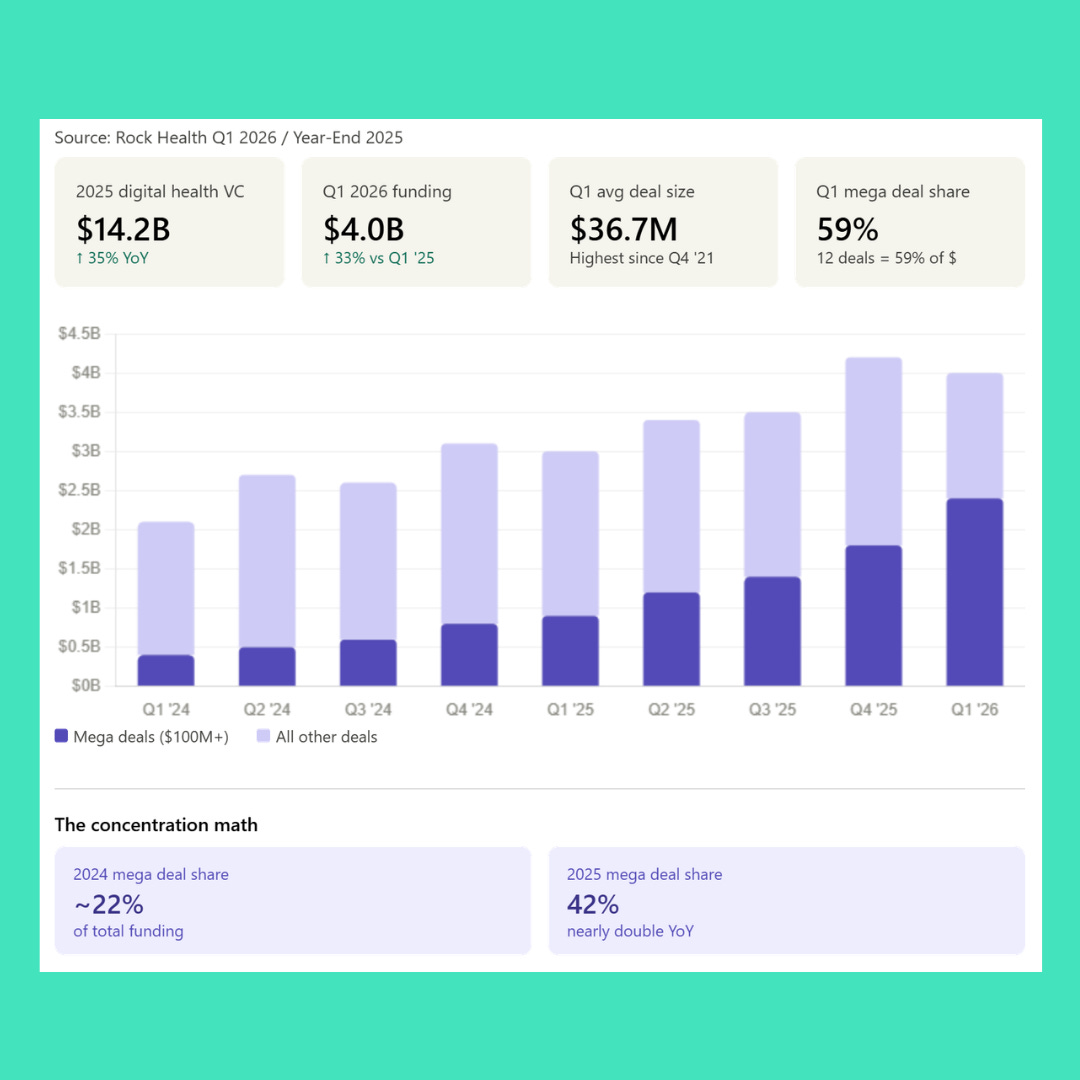

In Q1 2026, according to Rock Health, funding hit $4B, up 33% YoY. It was $4.2B in Q4 2025. And I don’t think folks were just trying to shrink their tax liability at the end of the year.

But here’s the thing. While there was more money dumping into “startups” it was dumping into fewer and fewer startups. And I put startups in quotes for a reason, which you will see in a moment.

The average deal size in Q1 2026 was $37M, the highest since Q4 of 2021, when we were riding high on anyone with a telephone and a multistate license just dumping money post covid. We also saw the share of mega deals, anything over $100M, double from 2024 to 2025. And in Q1 2026, 59% of all capital deployed was for mega deals.

Here’s the Frenchman’s chart:

That’s 110 deals total with 12 mega deals. What we’re seeing is capital flowing to fewer companies, but funds taking bigger swings on later stage companies that have shown a record of performance. We are also seeing companies stay private and continue fundraising longer.

Gone are the SPAC days (one hopes) and it seems we are back to a version of the good old days when companies with good mechanics IPO only when it makes sense as an organization, not just to make a quick buck. But as a result (and thanks to Omada and Hinge for snapping the dry spell) companies are still raising D and E rounds from venture firms.

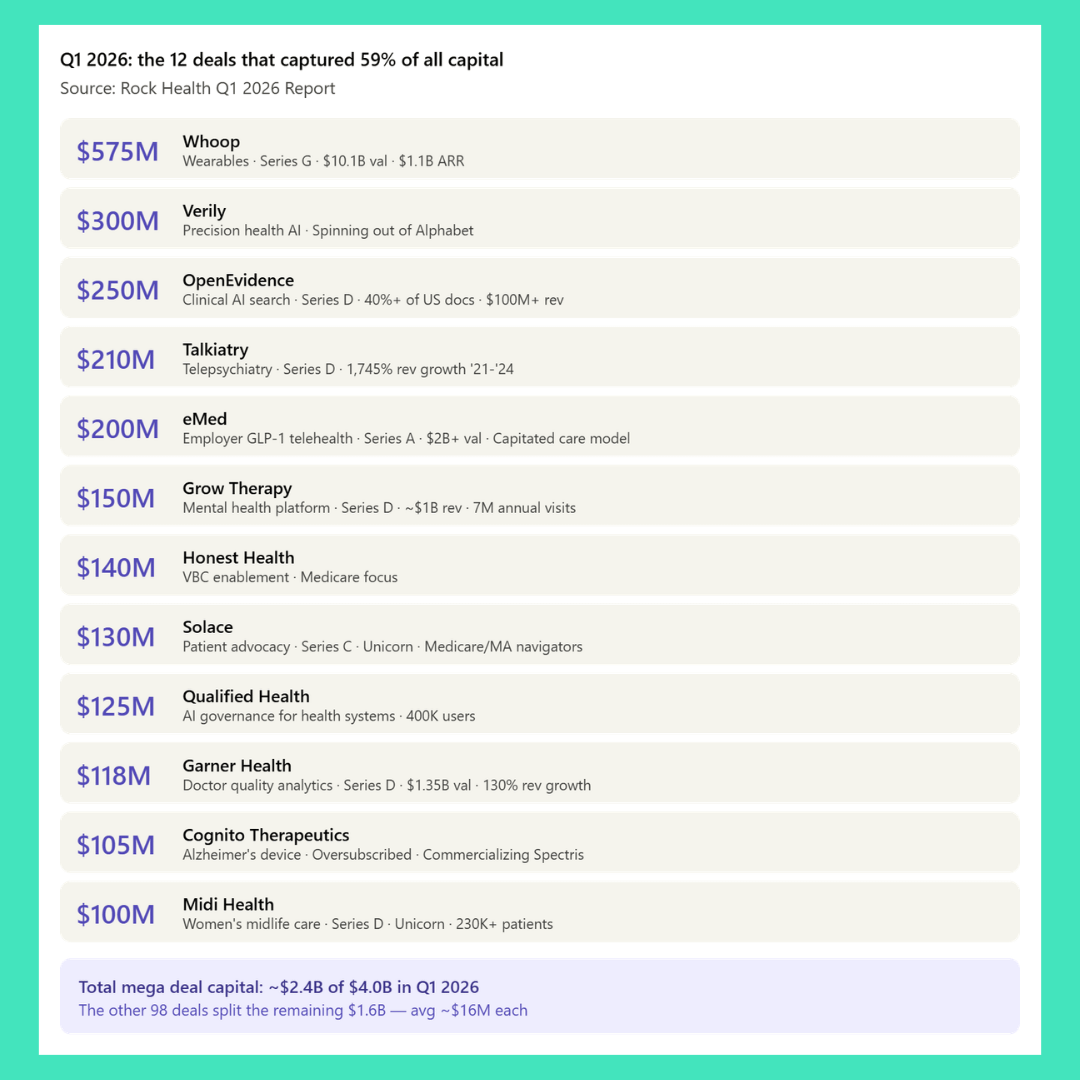

Here are the mega deals we recently saw:

And now you also see why I put “startup” in quotes. Whoop and your company that is a deck and 3 people are not startups in the same way.

And then for Private Equity, we’re seeing something similar-ish. See, the Barron Von Sweatervestensteins raised massive funds during the cheap money era of 2020-2022. Well, the LPs (limited Partners) have come knocking. The flip time for PE is 7 years on the outside. We’re closing in.

In 2025 we saw record Private Equity activity. 445 Buyouts worth $191B in deal value. On the other side, $156B in exits.

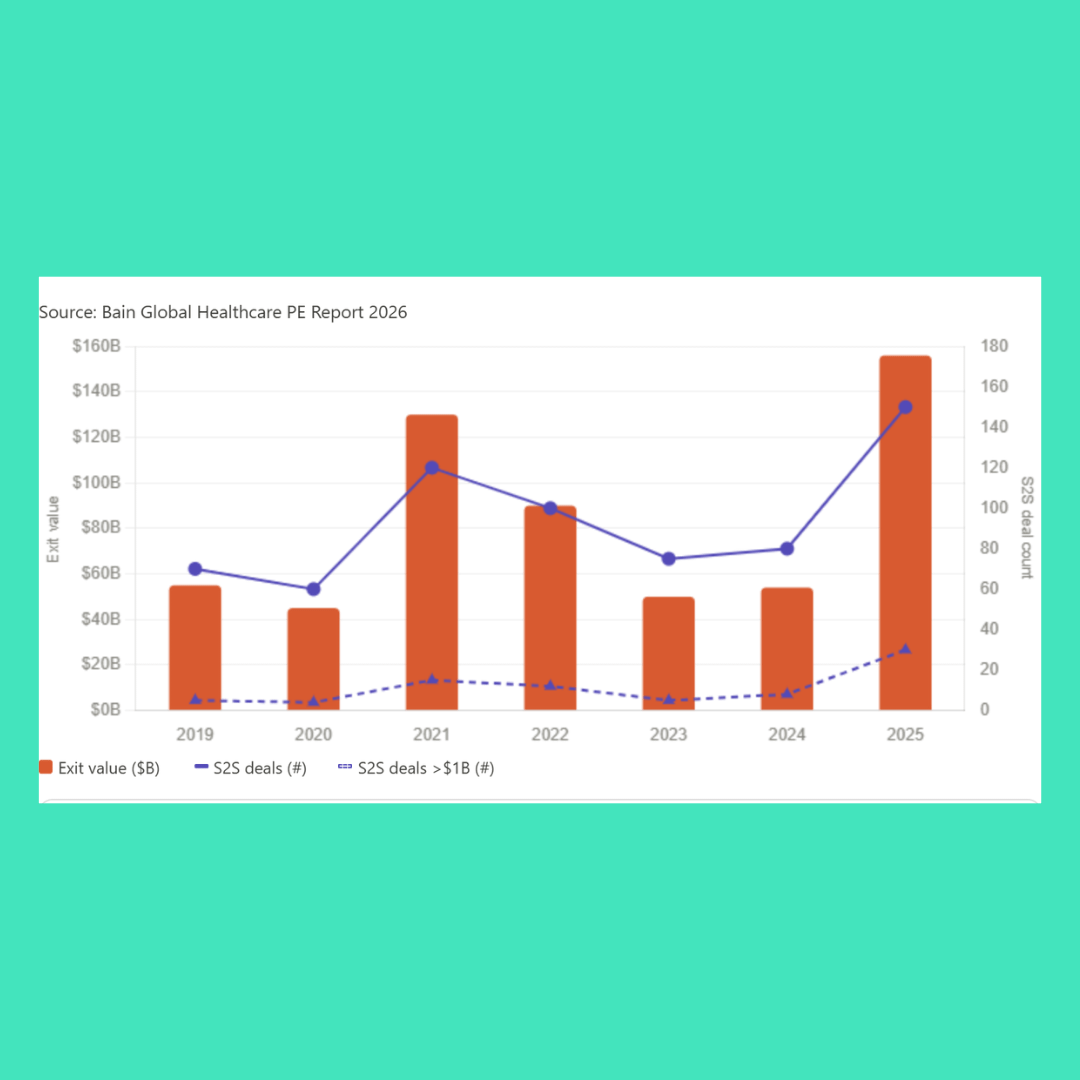

But the part that makes this so interesting is that of those exits, 150 of them were sponsor-to-sponsor (S2S). Meaning private equity selling to private equity. Barron McMoneyFace selling to Tripp Pennyloafer III. It underlines the pressure to exit and bring investors liquidity events as well as operators their proverbial second bite of the apple.

The S2S deal flow:

The dynamic will continue to be interesting as an estimated $1.1T is waiting to be deployed in healthcare alone. Now, that’s global across healthcare sectors, but that’s still a record high. It’s another reason why we are seeing so many S2S deals in the mix. They need to deploy capital and also get a cash return for LPs.

Another acronym, DPI or Distributions to Paid-In Capital has become the metric that matters most. LPs want the cash money man. Until they see it, their investments are tight, so new dry powder has well, dried up.

We’ve already been seeing it. PE fundraising has been declining for 3 consecutive years. Without a strong DPI, investments aren’t flowing like they once were. The record deal activity we are seeing right now is being fueled by dry powder from the 2020-2022 fundraising cycle. And the exits are from 2018-2020 portfolios. With those two dynamics, we may be heading for a much slower deal flow in the coming years. Certainly a more disciplined one.

Oh man, money is fun right?

And great. Thanks Preston, what does this mean for me? Well, I am getting there, I just like to paint a picture ok? I’ve been gone a while, I’m savoring the moment.

Here you go Mr. impatient:

If you are a founder: Deals are consolidating and whether VCs are more disciplined or are focused on the new shiny things, the dynamics have changed. Even with a proven track record, without a defensible position against the AI Armageddon you are going to be on an uphill climb. It’s never been an easy thing to do, but now more than ever, with companies staying in the ecosystem longer and more VCs looking to larger rounds, the need for real results cannot be understated.

If you are a practice: I’m not trying to be that guy, you know me, I’m not that guy, but the people buying have a lot of money to spend. They are looking for deals. The devil is in the details here, but if I can say anything, it’s make sure the deal is structured right, there is skin in the game, and that you haven’t sucked all the economic value out of your practice before you are ready to sell. Funds aren’t buying patient panels any more. They also may not be as motivated for long. $1.1T in dry powder sounds like a lot, but it’s spread across all of healthcare, and with fundraising declining three years running, the pipeline behind it is thinning.

If you are an investor: Exits are taking longer and longer. That means capital is not a short game anymore. Meanwhile LPs are looking for their paper. There is still value out there, but blindly buying or investing in assets to either roll up or are trendy aren’t going to get you there. This is about fundamental operations and value. Can you find it, run it, and expand it.

Welp, those are about all the words I have for today. I hope you are as glad to be back as I am. Tune in again for deeper dives into all of this. The S2S buying machine, the hundreds of companies in limbo with nowhere to go from a funding and exit standpoint, what’s the deal with all these IPOs, and much more.

I hope even more that you read this over a mimosa with Taylor’s new banger blasting in the background.

Oh, and Happy Father’s day to all the Rad Dads.

See you out there!

Welcome back, brother!

So glad to see you back! Incredible analysis!