The Healthcare Breakdown No. 068 - Breaking down Private Equity’s healthcare deal mechanics part Uno

Brought to you by Double reverse draw 2

What we’re breaking down: Sponsor-to-Sponsor deals in healthcare

Why it matters: Knowing the motivation and mechanics in the private equity exit is leverage

Read time: The time it takes to regret SPF 15 when you needed 50… (7 minutes for real though)

If you joined us last week, which you better have otherwise we can’t be friends anymore, we talked about the money in healthcare investing.

We covered two big buckets and different perspectives. The buckets were Venture Capital, those guys wearing zip up North Face fleece vests and Private Equity, those guys wearing zip up puffy Patagonia vests. And no, I don’t know why rich finance people never have cold arms.

The perspectives we covered were the seller, the limited partners, and the investors. Today, and for the next three issues (that’s right you are in a four parter!) we are going to talk about private equity.

Now, if you have been here before, you have read issues on Steward Healthcare, how private equity works from a structuring perspective, and private equity strategies. I told you The Breakdown is getting a glow up, so we are taking a beat on railing against the evils of Private Equity and focusing on the mechanics.

Because, and importantly, when you understand the mechanics you can eschew the allure or you can leverage it. Both are valid. We shall leave the philosophical musings to another day. You can call me toll-free any time.

Here’s how it’s gonna go:

Part 1: (you are already in this part, thank you for being awesome) The Sponsor-to-Sponsor machine

Part 2: The anatomy of a deal

Part 3: When the mechanics fail and the machine breaks

Part 4: When it all comes together and the machine makes a Wonka bar

Let’s go!

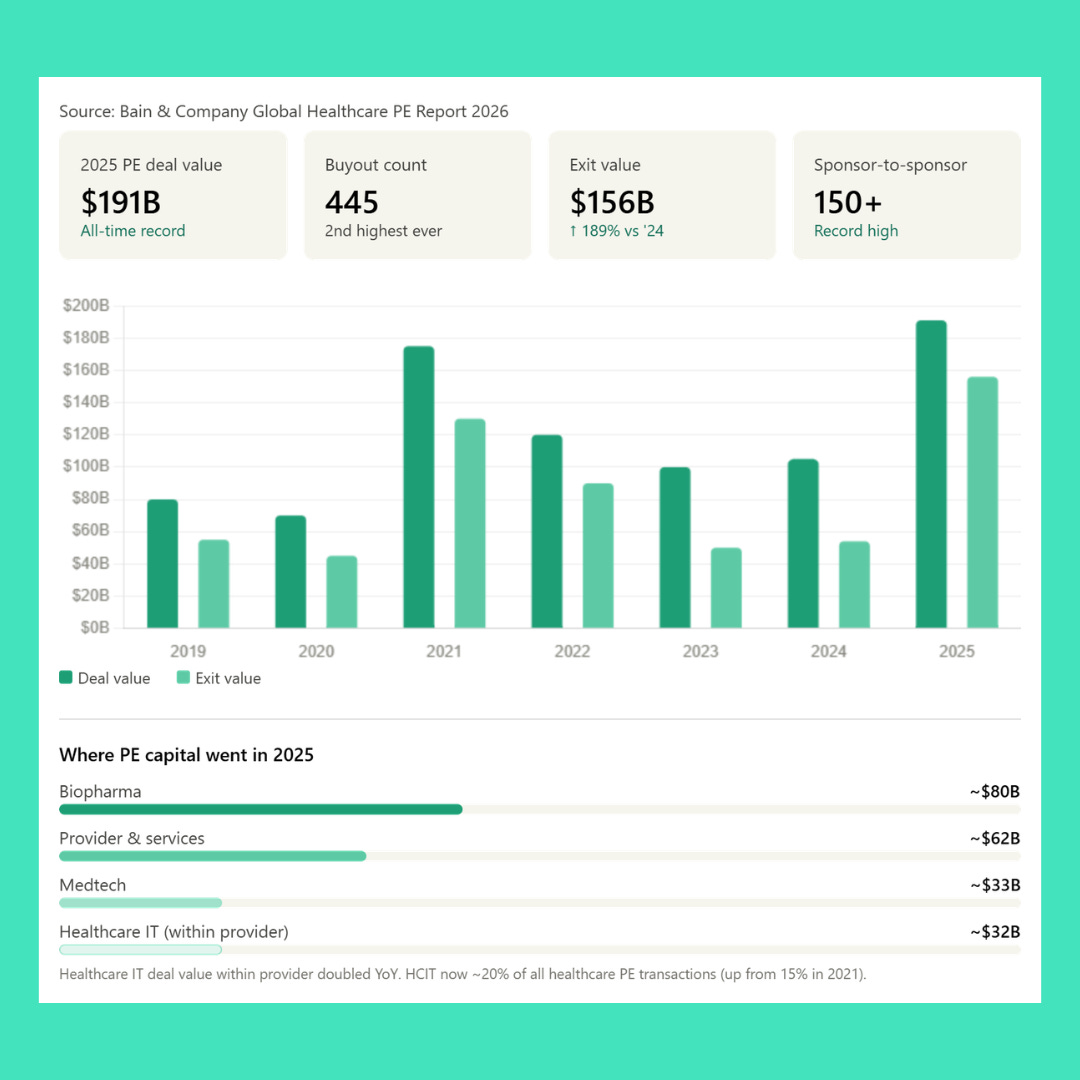

In the last episode we covered the macros, as mentioned above. To refresh you memory like a Frutopia on a hot 1997 evening, you saw this fancy new graphic, which shows $191B in deals, $156B in exits, and $1.1T in dry powder:

We also talked the Distribution to Paid-in-Capital pressure and declining funding as a result. If you haven’t, I 50% recommend you go back and read it here.

Now, let’s look closer at the Sponsor-to-Sponsor deals that are happening.

But first! What is a sponsor-to-sponsor deal and why is it happening so much more now than ever before?

Simply enough a private equity firm is a sponsor. When there is a PE backed acquisition that is sold to another PE group, it’s one sponsor selling to another. Shorthand because business people are wildly imaginative, is S2S. Tee, double ewe, oh, is just 2 much to spell.

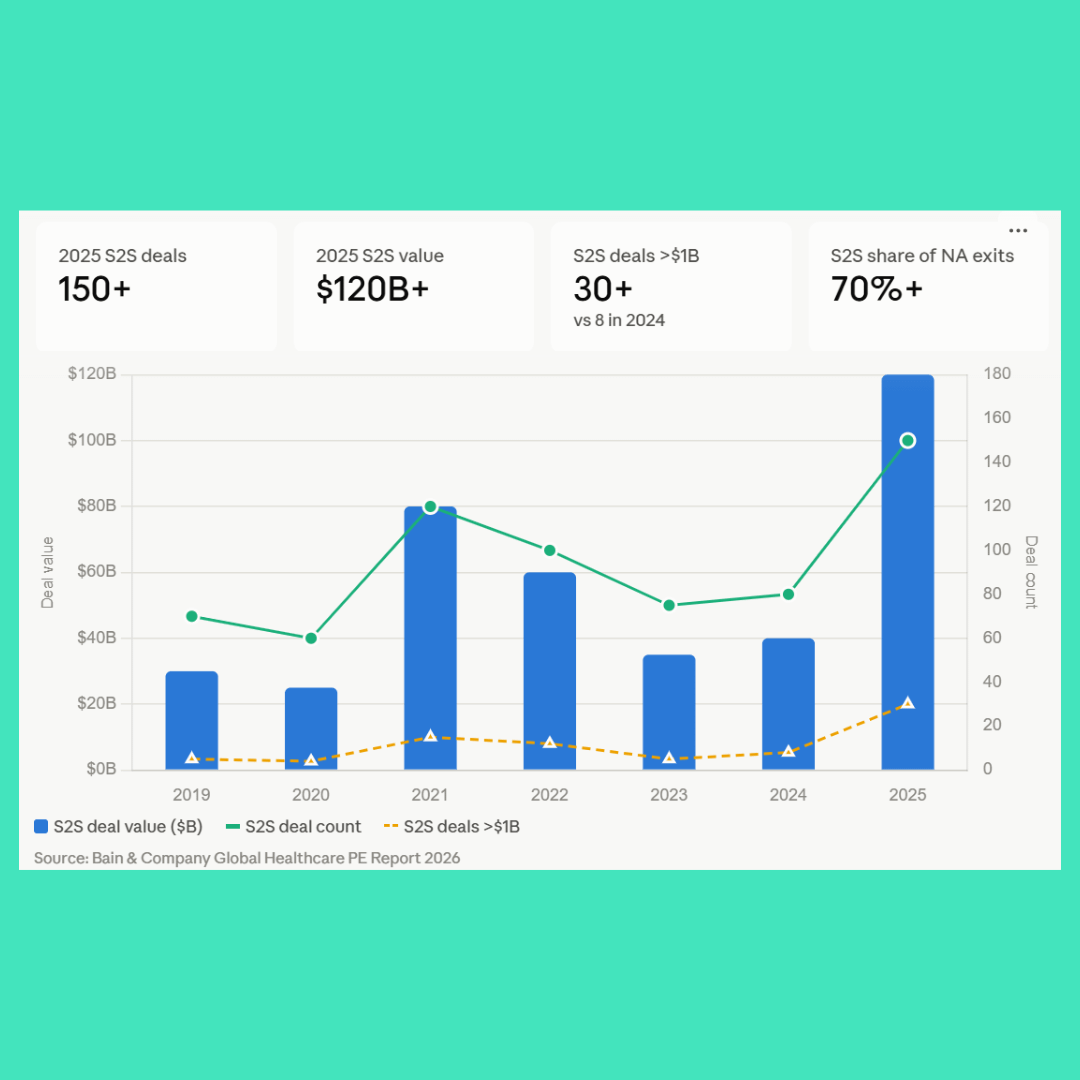

Here’s how well oiled the money machine has gotten…

In 2025, there were over 150 sponsor-to-sponsor healthcare deals worth more than $120 billion. Over 30 of those exceeded $1 billion. And more than 70% of North American healthcare PE exits last year were S2S.

It’s even more pronounced in physician practices. A 2024 study published in Health Affairs Scholar looked at 807 PE physician practice acquisitions and found that 98% of exits were secondary buyouts.

More charts:

And why is all this selling to friends and family happening?

Back in the good old days, when your company was big enough and you needed capital infusions, you went to the public capital markets. You would call up your friendly neighborhood investment banker and they would take you on the road to shill your wares so that when you went public everyone who was cool wanted to buy your stock. The result was a large amount of capital in your coffers and a host of new headaches for your PR and legal departments.

Well, when Sarbanes and Oxley got together and the Lehmans decided to FAFO, the IPO market changed. While in a way it still remains the pinnacle of company velocity, it’s not as straight forward as it once was. There are also more alternatives. Well, one big one, but a lot more private equity than there used to be.

So, instead of rolling the dice in public markets, you can sell to private equity, take chips off the table, and go through a more predictable, faster transaction. We have seen hundreds of billions in private equity deals over the last 10 years.

Another avenue other than IPO is strategic acquisition. Think Pfizer buying your anti-toe-fungus drug that comes in eye drop form or Stryker buying your middle finger extender total joint. And those are still happening. You should actually probably call Zimmer, they love buying things.

Side quest: if this is your line of business, you should be trolling public filings for similar acquisitions and also see how much cash sits on balance sheets. That’s the dry powder for strategics.

But, for the healthcare services and digital health side of the world, it’s a little different. Strategics are health systems or perhaps other large service providers. Health systems come with their own bag of tricks and baggage. Increased regulatory gymnastics, payer battles that never end, fierce competition, capital constraints, and all that fun.

As for the larger companies in the same services areas, namely other digital health, health tech, etc. they are dealing with the same, “what do we do now,” dynamics.

Taken together, this leads to more volume in PE groups buying from one another. And as we discussed last time, PE is under pressure to deploy capital and to produce returns on currently deployed capital. Not uncommon, but the cycle is pronounced since the cheap money days of yore.

We also see specialization happening in Private Equity. In the same way it used to be cool to be a VC that only does seed and series A, private equity is small business, micro business, small-medium size, extra medium, and super double secret size. It runs the spectrum. And thanks to Codi Sanchez, your uncle Henry is now a laundromat private equity wiz.

Here’s a simple example of the cycle. Langdon Thompson III buys your company. He finds 2 more bolt on acquisitions and sells to Lord Pennington Woolsworth for 12x EBITDA, who then scales to 6 states. Then Maestro Charles Hethingford the 19th of Buckheadshire buys the platform to hold, optimize and either take public, create a continuation vehicle, or chop it up and sell it for parts.

It can be argued that none of this is value creation, it’s more arbitrage and financial tomfoolery, but there are worlds, as we will see in future episodes in this series, where this plays out for the better. Where sponsors invest, creating technology, expanding access, investing in growth the right ways, where this all pays off.

No, not you Steward Health Care…. Can’t even spell healthcare right…

Here are some real instanced of the second and third sales of healthcare services:

Forefront Dermatology. They’ve been through three sponsors. Varsity Healthcare Partners built it, sold it to OMERS in 2016, who doubled the footprint and sold it to Partners Group for $1.5 billion in 2022. Physicians and management rolled equity each time. Three sponsors deep and now the largest single-specialty physician-led derm group in the country with 200+ practices.

That’s a lot of moles.

Or my hometown favorite, EyeSouth Partners. Shore Capital formed it in 2017 with one ophthalmology group. 5 locations, 12 doctors, about $2 million in EBITDA. Five years later, 155 locations, 270 doctors, 11 states, EBITDA north of $70 million. Sold to Olympus Partners for just under a billion dollars. The founding physician became Chief Medical Officer and the doctors who rolled equity got their second bite at a $1 billion valuation.

Headlands Research, Epiphany Dermatology, DOCS Dermatology, to name a few more, are all S2S. In derm alone there are now 35+ PE-backed platforms across 20 states.

Between investment and exit, PE firms increased the number of affiliated practice locations by an average of 595%. The machine rolls on faster than a Little Debbie at your nephew’s 5th birthday party.

The point for today is this: once a practice enters the PE ecosystem, the data says it’s almost certainly not leaving. It’s going to pass through 2-3 sponsors over the next decade. It’s kinda like when you are almost 40 and you keep going through cycles of getting back in shape like you were in your prime. Not that I would know anything about that… At the end of the day you keep resetting and it takes 5-7 years, three times.

In the next issue we’re gonna go deep into the deal math. How the multiple arbitrage actually works. What gets bought, at what price, who gets paid at exit, and what happens when the next sponsor shows up at 12x and has to figure out how to make their own returns. If you want to read the word EBITDA over and over again, that’s going to be the issue for you.

I would also be remiss not to mention that Taylor Swift got married this weekend and I hope you had an amazing America’s birthday. May the odds ever be in your favor as you spend the afternoon working through your hangover with 7-12 mimosas. Either from the birthday celebration or Taylor’s celebration. Both valid.

See you out there… America.

As always, incredible insights!