The Healthcare Breakdown No. 059 - Breaking down how insurance makes all the money from doing nothing at all

Brought to you by the revolution aka The Association for Independent Medicine

What we’re breaking down: Health insurance float

Why it matters: Health insurers are denying claims and delaying payment to protect float

Read time: As long as it takes to get too full from IHOP’s endless pancakes (6 minutes for real though)

I think we can all agree, insurance companies suuuuuuuuuuuuuck. Like they really, really suck. Healthcare costs the US $5T and 5 health insurers rake in about $900B of that.

20%.

5 companies.

But first, a word from our sponsor!

As healthcare becomes increasingly consolidated, with large hospital systems and corporate entities gaining greater control over healthcare, the Association for Independent Medicine (AIM) counterbalances this trend. It champions the belief that independent medical practices — led by physicians who own and operate their practices — offer unique advantages in terms of patient care, healthcare costs, and physician autonomy.

AIM was created in 2022 to advocate for the autonomy of healthcare professionals who want to maintain control over their practice without the influence of corporate medicine or hospital systems. The organization’s mission is multifaceted: it provides resources for physicians and other healthcare professionals to navigate the challenges of running their practice, advocates for regulatory and policy changes, and fosters a network of like-minded professionals who believe in the importance of patient-centered, personalized care. Open to all specialties, AIM offers both group and individual memberships. More info can be found at www.associationforindependentmedicine.org.

DARN RIGHT! Love those guys. They’re doing great things. Call them. Like right now.

Ok, back to the rafts.

The float we are here to talk about, is insurance float.

First of all, what the heck is it? Why does it matter? And how can you get you some?

Foray one: what is it?

It’s this:

It’s also this:

For those keeping track, this means…

UHG

Working capital ($20.6B)

Current ratio: 0.79

Cigna

Working capital: ($11.4B)

Current ratio: 0.77

From first glance you may be asking, why in the world does UnitedHealth Group, the largest and most nefarious of all insurers, owe more money than it has?

Isn’t that a problem?? You spend all these Healthcare Breakdown issues telling us about why you shouldn’t get overleveraged, managing cash, and all kinds of boring conservative stuff and now this???

Wait, don’t go!

First of all, check this out:

Sorry for the tiny writing. See, one more reason to hate insurance companies. They make everything harder.

It’s easy to see that while it may seem like a problem, these two puppies are doing just fine. And by puppies, I mean large, soulless, evil empires.

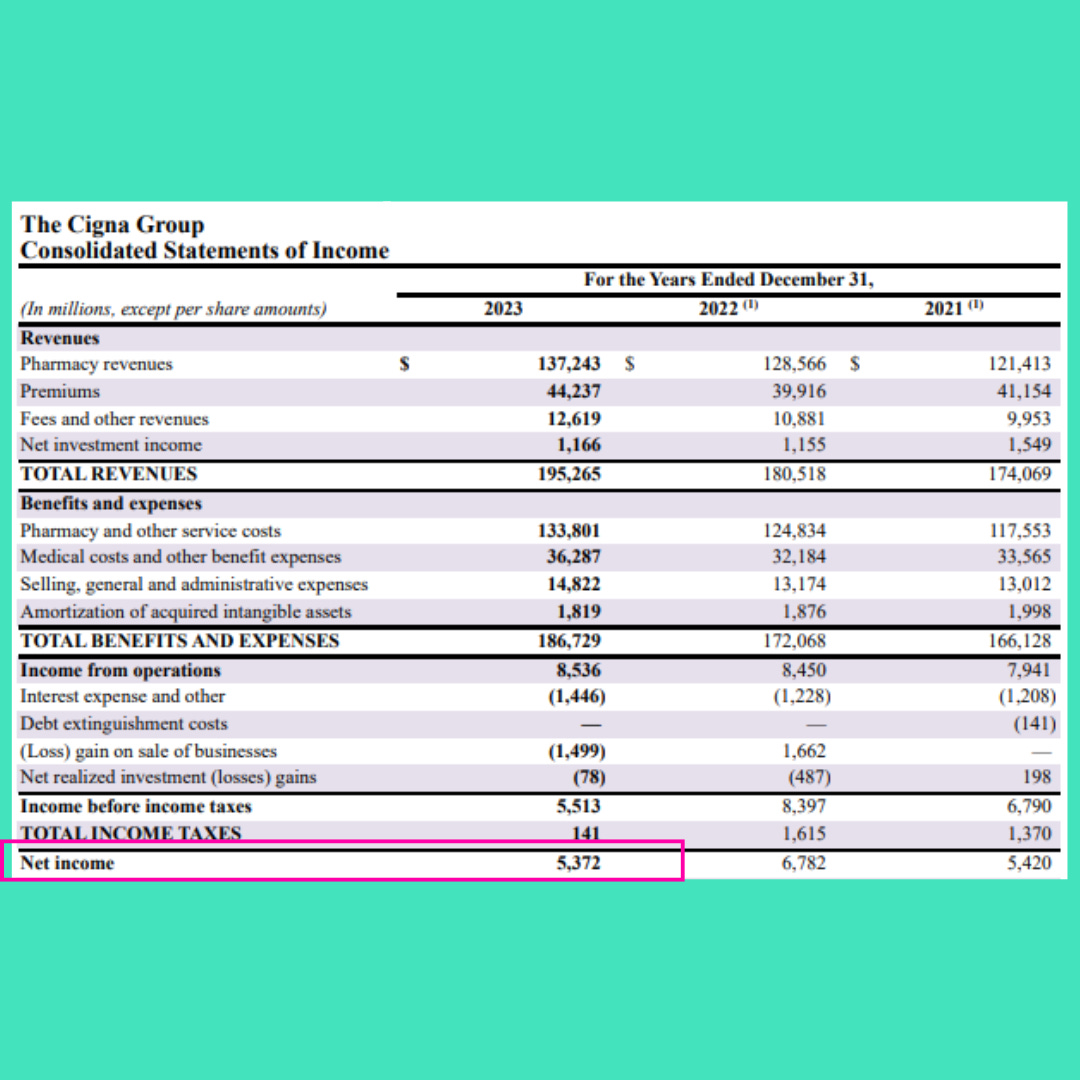

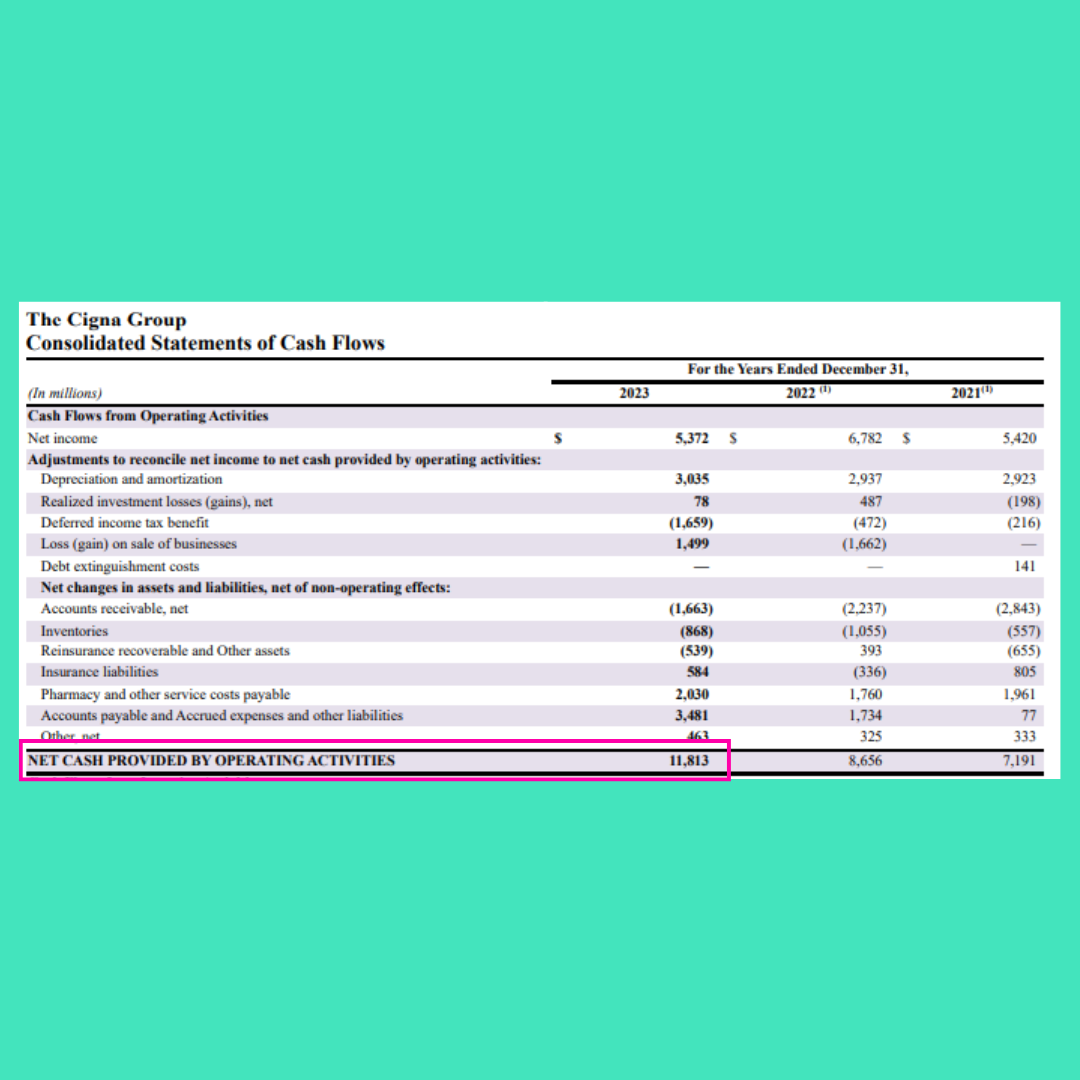

Cigna made a TON of money and UHG made even more TONS of monies.

So, what IS going on then? How do they owe all this money but still make so much money??

Well, insurers in their infinite wisdom and trickery use something called float.

And it’s all about this:

And this:

What you are looking at is cash received but not yet paid out. Cash that these insurers have, but owe. Later.

The dark arts is in the “later” part.

Here is how it works:

You pay your premium.

UHG’s 7,900 actuaries estimate how much you are going to cost them over the next year.

That number, the estimate, goes onto the balance sheet as a LIABILITY. It’s not an asset because it’s money they will eventually pay out.

Key word: eventually.

As in, you pay them $400 bucks this month, they keep $60, and record $340 as a liability. To be paid at some point in the future.

Here is the magic though! They don’t just let that money sit on an old dusty mattress in their Scrooge McDuck money vault to go swimming in on the weekends.

They put that money to work. They invest it. They buy stuff with it. They use that money to make more money.

Then, eventually, after they have denied your claims as many times as possible to prolong the eventuality of payment, they pay that $340 out.

But, unbeknown to you, that $340 is now worth $470.

Free money.

What looks like a liability to you and me, is free money for them. Your money.

It’s all about timing.

Which brings us to…

Side quest 2: Why does this matter?

It is literally (am I using this word right? Maybe it doesn’t mean what I think it means…) the underlying cause of so much of our insurance woes.

Remember the “eventually” part?

That’s the whole game. The longer an insurer can wait to pay you out, the more money it makes.

What does that look like for you and me?

Denying MRIs ordered by your physician. Denying medications you need. Denying surgeries. Denying treatment that couldn’t be more medically necessary.

Denials for the sake of delay.

Insurers will do anything to protect the float. And unfortunately, it’s not the good kind on the Hooch. It’s the evil kind.

And that’s all I have to say about that.

Final countdown: How you can do it for good, not for evil.

Remember your best friend, Cash Flow and why it’s so important?

The reason is timing. It’s also why float is powerful.

Sure, you owe that money, but not yet. What can you do with it to grow it before you owe it?

Ohhh my. I like that. “Grow it before you owe it.”

Trademarked! Can’t steal it! You heard it here first. Where’s a lawyer?

Freakin lawyers, never there when you need one, always there when you absolutely don’t.

Here’s how you can apply the concept.

Find ways to get your revenue upfront to deliver a service or product later.

Practically speaking that could look like preselling 4 month’s supply of something upfront to be delivered over the coming 4 months. Use the money to get more customers, more product, or invest in something else.

Discount memberships for the full year so you receive payment upfront but deliver over the coming 12 months.

Bundle services that someone will use over time, but the cash is received before services are delivered.

Here’s a picture of the concept. Cause I know you love hot pink pictures:

(By the way, ignore the simplicity of how revenue hits a balance sheet. This is just for illustrative purposes.)

In this totally made up example, you have a customer who pre-pays in some way for the service or thing you sell.

$613 of those dollars are a liability since you owe delivery on something worth $613 later. But there is nothing keeping you from using all of that money to get the customer flywheel going.

Since you are savvy AF, you use that money to get more customers to pay you upfront, to get more customers to pay you up front, to get you more customers to pay you upfront, to…. I think you get my point.

Customer financed customer acquisition.

That’s one way to adopt the concept. In insurance land it’s use premiums that should be paid out in covered services to buy more investments from your bestie’s private equity fund and stock buybacks to increase returns and share price to get a bigger bonus and higher profits.

I mean, tomato, tomahhhhhhtoh (phonetic spelling of snarky posh British accent).

And while you may not be operating in the financial sense of float, the concept can be applied in the same way insurers use it.

Get max money upfront and then grow it. Be careful not to overextend it. This isn’t a Ponzi scheme. This is a focused way to grow through customer financing.

Use this tool for good. Not for evil.

By the way, unrelated side note… let’s stop calling insurers, “payors.” They are processors. And gate keepers. It’s your money, not theirs. They don’t pay for anything. They take. You pay.

Love you.

Would like to talk Dr Keith Berger MD in VA Beach keith@rewritethefuturenow.com

I’d push on this a little. Framing the current funding environment around raising a seed round or selling a practice feels a bit narrow when the more meaningful impact is often what it changes operationally before a financing or exit is even on the table. Capital pressure shows up in strategy, partnerships, headcount, outsourcing, and consolidation decisions first.